Theme: Principal-protected exposure to the worst performer of Gold or Copper (USD)

Term: 24 months · Protection: 95% at maturity (issuer guaranteed*)

Upside Participation: 170% of the worst performer’s positive return

Performance Cap: 30% (maximum payoff reached at +30%)

Averaging Out: Final 2-month averaging window

Currency: USD

Max Return: 151% of capital (100% principal + 30% × 170% = +51%)

Returns and protection apply at maturity and are subject to issuer credit risk. Early exits may differ materially.

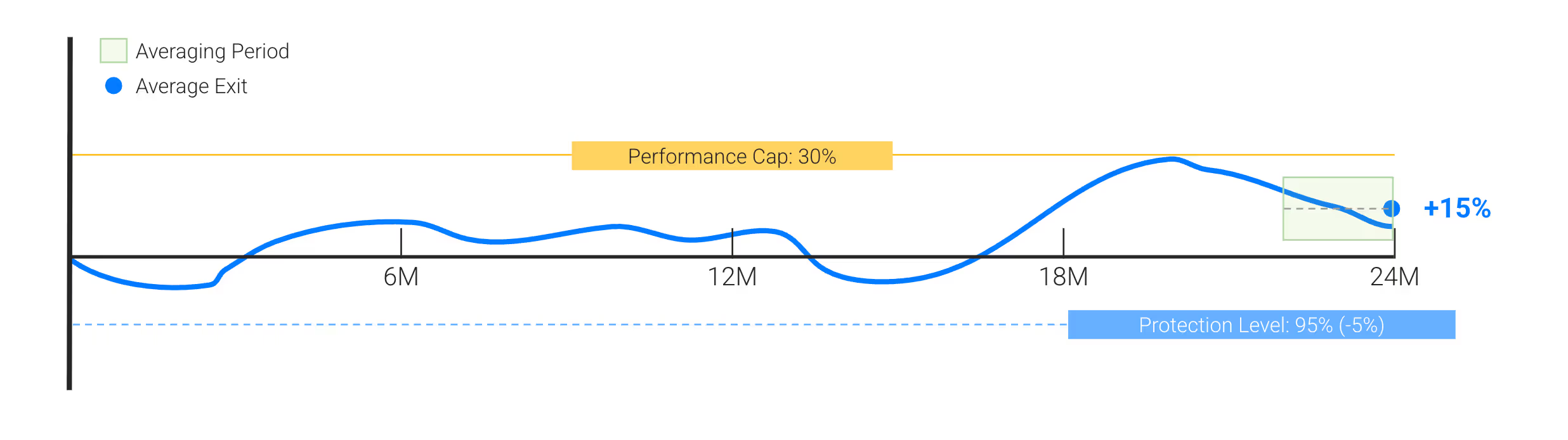

1. Bullish (below cap): Worst performer +15% → Return = $1,255,000

Calculation: $1,000,000 + (15% × 170% × $1,000,000) = +$255,000 (+25.5%).

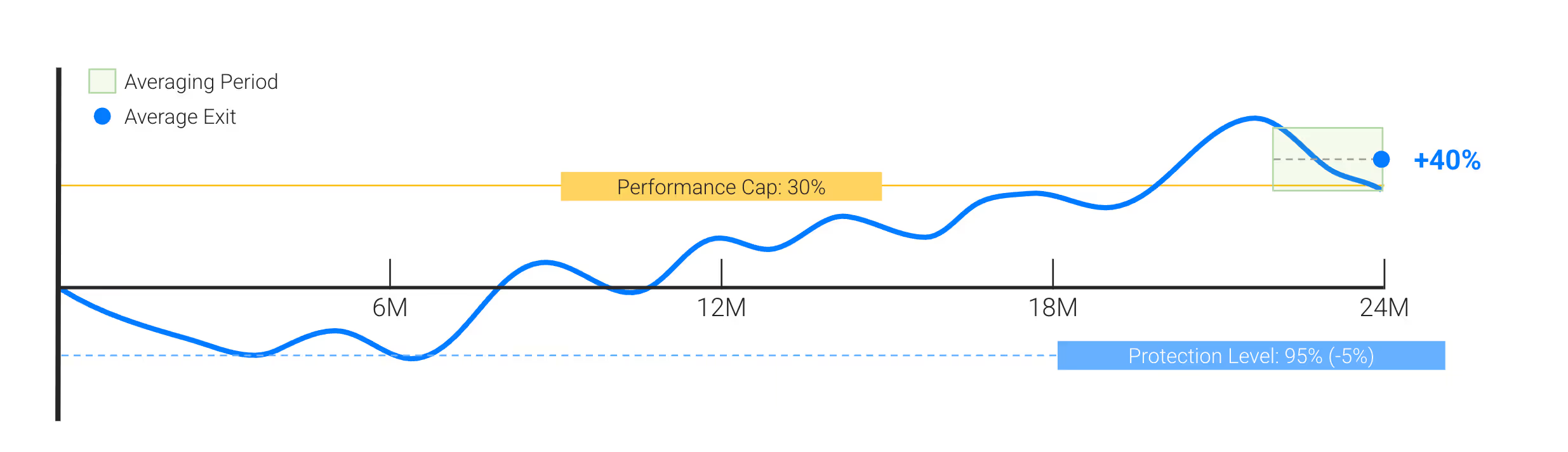

2. Very Bullish (above cap): Worst performer +40% → Capped at 30% → $1,510,000

Calculation: $1,000,000 + (30% × 170% × $1,000,000) = +$510,000 (+51%).

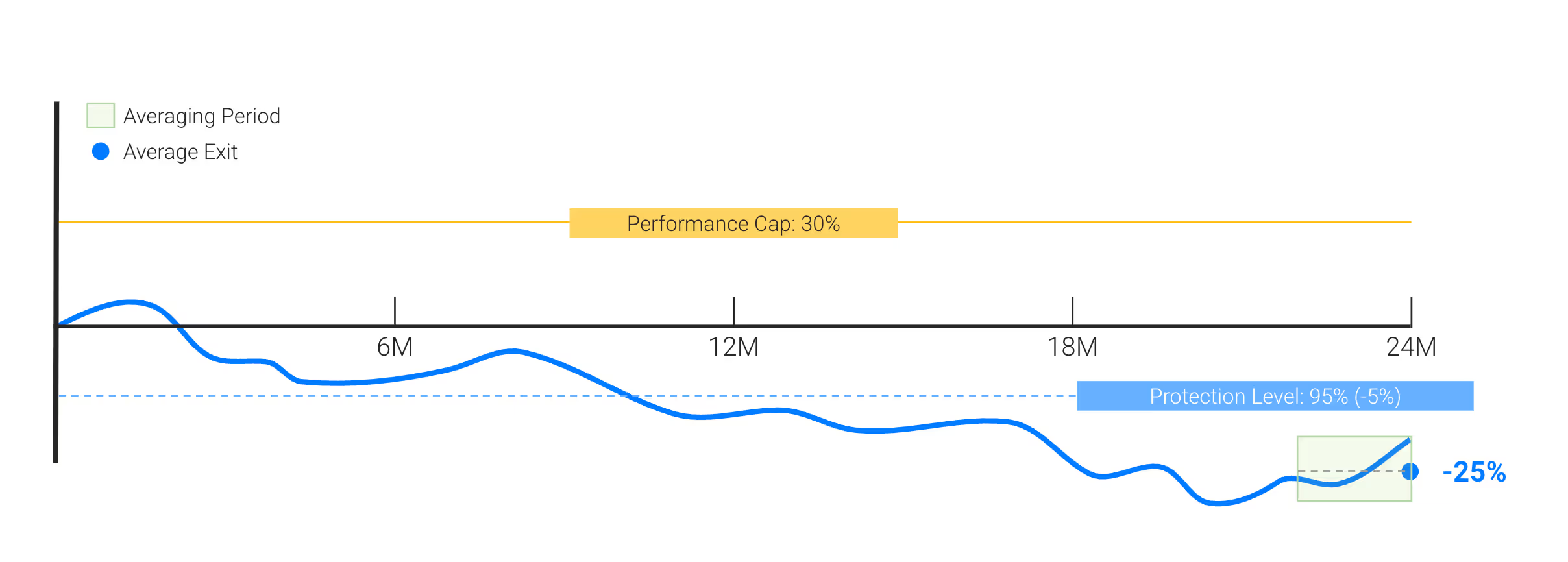

3.Bearish (below protection): Worst performer –25% → $950,000 back at maturity

Outcome: –5% (protection level).

The note combines a discounted bond (to secure the protected amount at maturity) with options that provide market exposure. Higher protection generally means lower participation or an upside cap—that’s the core trade-off.

.png)