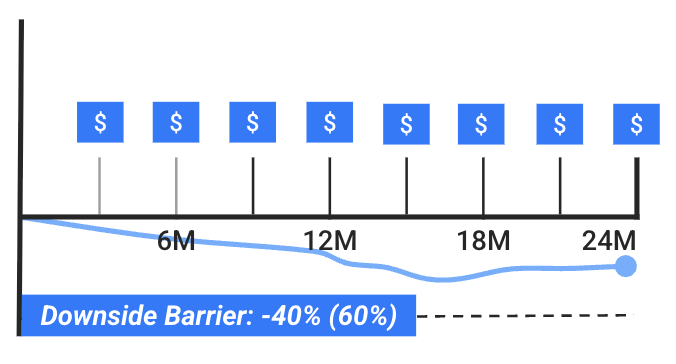

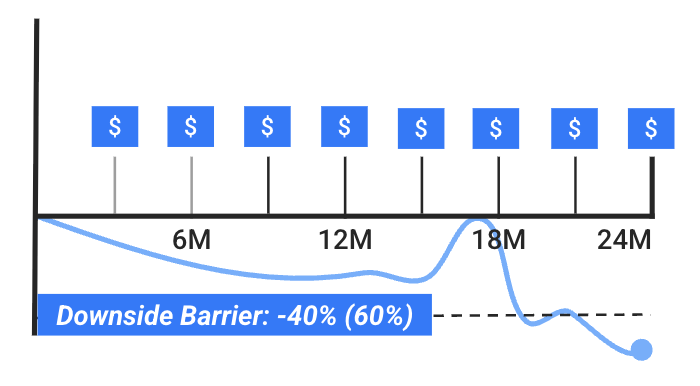

A Fixed Coupon Note (with Barrier) is a common variation of Barrier Income Note. It pays a fixed coupon regardless of asset performance1. Capital is secured as long as the reference assets do not breach the ‘downside barrier’ at maturity.

Scenario 1: Bearish Market

Barrier not breached at maturity: +16.00% ROI

Scenario 2: Very Bearish Market

Barrier breached at maturity: -19.00% ROI

The investments showcased in this example represent just a sample of the capabilities of Stropro. Structured investments solutions are highly configurable; our investment desk its able to tailor to reference assets, tenors, major currencies, combine features, and blend objectives to deliver tailored outcomes for you clients.

.png)