.png)

Markets are at or near all-time highs.

Equity concentration risk is elevated.

And client conversations are increasingly dominated by the same question:

“Should we invest now, or wait?”

For advisers, this is no longer a simple market-timing debate.

It’s a question of entry risk, behaviour, and how to deploy capital intelligently when valuations feel stretched.

Because while markets tend to rise over time on average, clients don’t experience averages — they experience outcomes, volatility, and regret.

Lump-Sum vs Dollar-cost averaging (DCA): Managing Market Entry Risk for Advisers

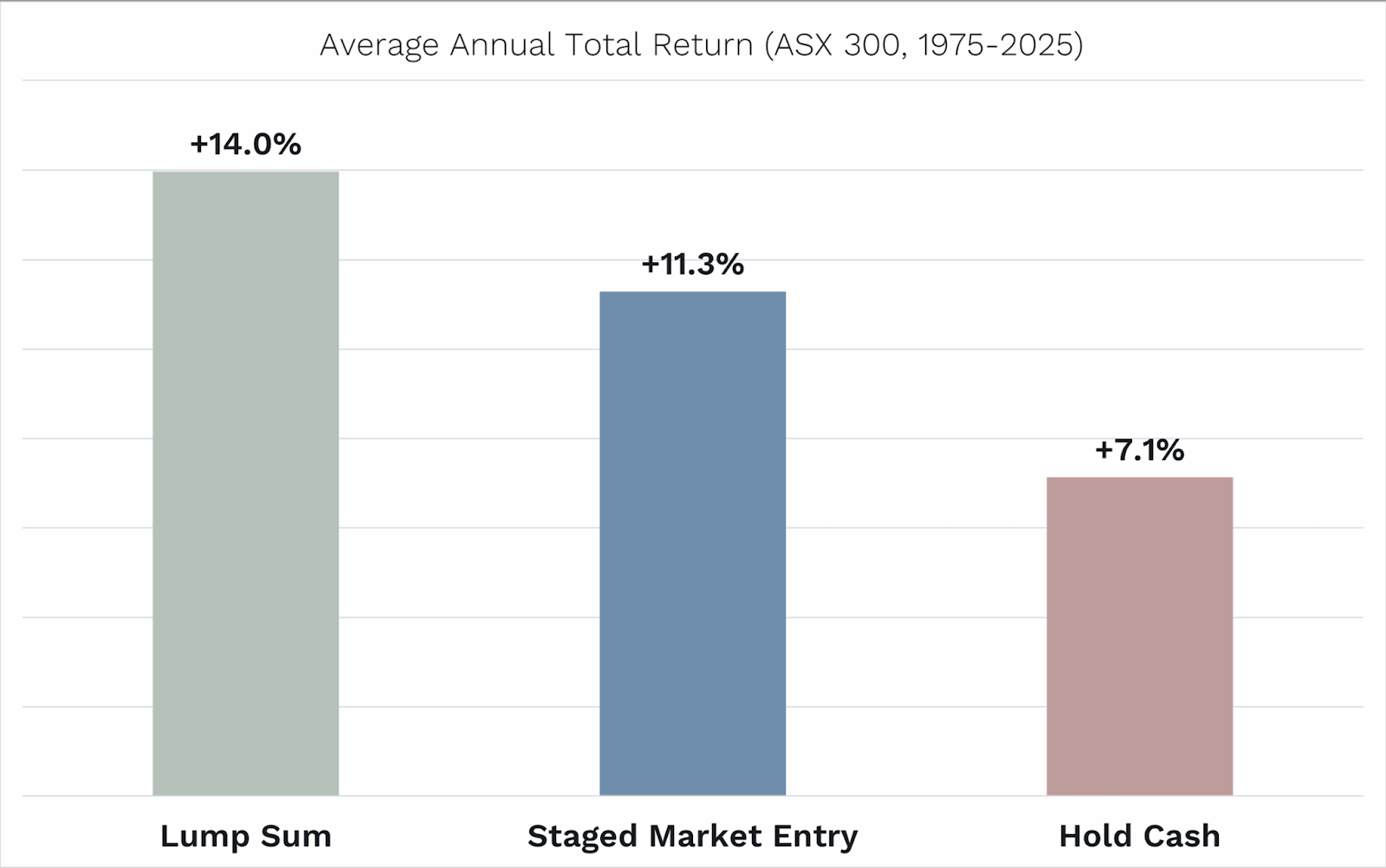

Decades of data show that lump-sum investing (investing all at once) typically outperforms DCA / staged market entry over long periods (four equal investments at the start of each quarter over 12 months). This is because, markets trend higher, and delaying investment often comes at a cost. See chart below.

But advisers don’t just manage portfolios, they manage people.

At market highs, the real risks aren’t just mathematical. They’re behavioural:

- Investing too aggressively and facing immediate regret if markets pull back

- Sitting in cash for too long and missing ongoing upside

- Freezing altogether, waiting for a “perfect” entry that never arrives

As one adviser put it:

“Clients say they’ll buy the dip — but very few actually do when it happens.”

This is why averages can be misleading.

They mask the tail outcomes that derail discipline and confidence

At market highs, the challenge becomes:

- How do we maintain exposure?

- How do we avoid poor timing at the start or end of an investment?

- How do we keep clients comfortable enough to stick with the plan?

Increasingly, private wealth advisers are answering these questions structurally, not emotionally.

Using Structured Investments to Manage Market Timing Risk.

Rather than choosing between “all in” or “sit in cash”, some advisers are using structured investments to reshape how risk is taken.

These approaches don’t remove risk, they change how it is experienced.

The goal isn’t to predict market movements, but to reduce sensitivity to short-term volatility — particularly when markets feel extended.

This allows advisers to stay invested without relying on perfect timing.

1. Capital-Efficient Investing: Staying Exposed Without Overcommitting Client Capital

Advisers are using enhanced growth notes to:

- Deploy smaller amount of capital outlay without sacrificing upside exposure.

- No margin call risk.

- Exposure in AUD to avoid cross-currency hedging.

- Defensive features to reduce timing or sequencing risk.

Lookback and Averaging Features

This growth-oriented strategies can incorporate:

- Lookback entry mechanics, where the entry level is set at the lowest daily close over an initial observation period.

- Average entry and exit pricing, which smooths exposure at the start and end of the term.

As one adviser explained:

“Capital efficiency doesn’t mean you can’t add exposure elsewhere — it’s all complementary in the broader strategy…Knowing that not all capital is tied up and that downside parameters are defined — often gives clients the confidence to stay invested.”

At elevated valuations, liquidity has value. Capital-efficient enhanced growth notes allow advisers to:

- Maintain market exposure

- Retain capital flexibility

- Allocate remaining funds elsewhere in the portfolio

This flexibility becomes particularly important for:

- Retirees seeking stability

- Pre-retirees balancing growth and control

- HNW clients who value optionality

2. Smart-Entry Notes: Getting Paid for Patience in Overvalued Markets

Another approach taken by top advisers are “paid-for-patience” strategies with Smart-Entry Income Notes.

These structures are designed for environments where:

- Markets appear fully valued

- Clients want income

- Advisers want to avoid committing capital at today’s prices

How Smart-Entry Notes Work

A Smart-Entry Income Note typically:

- Pays a fixed coupon (income paid monthly/quarterly regardless of market direction.

- Exposure to a single asset or basket of assets

- Includes a pre-set entry level (Smart-Entry) below current market prices

If markets remain above that level, investors:

- Receive their coupons

- Get 100% of initial capital invested back at maturity

If markets fall and the smart-entry level is triggered at maturity:

- Investors acquire the asset at the smart-entry level (discounted level)

- The coupons received over the term help add to the total return and if there is a sever sell off, soften the impact of the drawdown.

In effect, clients are being paid to wait — rather than sitting in cash waiting for a market correction to occur.

Why this Solution Resonate With HNW Clients

For many HNW and retired clients, the appeal is not chasing upside at any cost. It’s about control.

- Growth strategies provide exposure

- Capital efficiency preserves liquidity

- Smart-Entry notes generate income while waiting for better prices

Importantly, clients know:

- What can happen

- What can’t happen

- And how much risk they are taking at the outset

As advisers often find, clarity around downside matters more than upside projections.

Elevate your advisory services

If you are a private wealth adviser we invite you to book a consultation with our team to explore how to utilise institutional-grade structured investment solutions to deliver personalised, outcome-defined strategies for high-net-worth clients.

.png)

.png)