1. At the beginnning of the term, Investor posts shares as collateral and borrows at a 70%-90% Loan-to-Value ratio (LVR) of the shares' value in AUD (or preffered currency).

2. Depending on market performance and personal preference, investors at maturity:

Assumptions:

A) Keeping Shares at Expiry

1. Bullish Market: Share price above the call strike. (116% of intial price):

2. Neutral Market: Share price is between 80% and 111% of initial price.

Options at maturity:

3. Bearish Market: Share price below the put strike. (70% of inital price)

B) Selling Shares at Expiry:

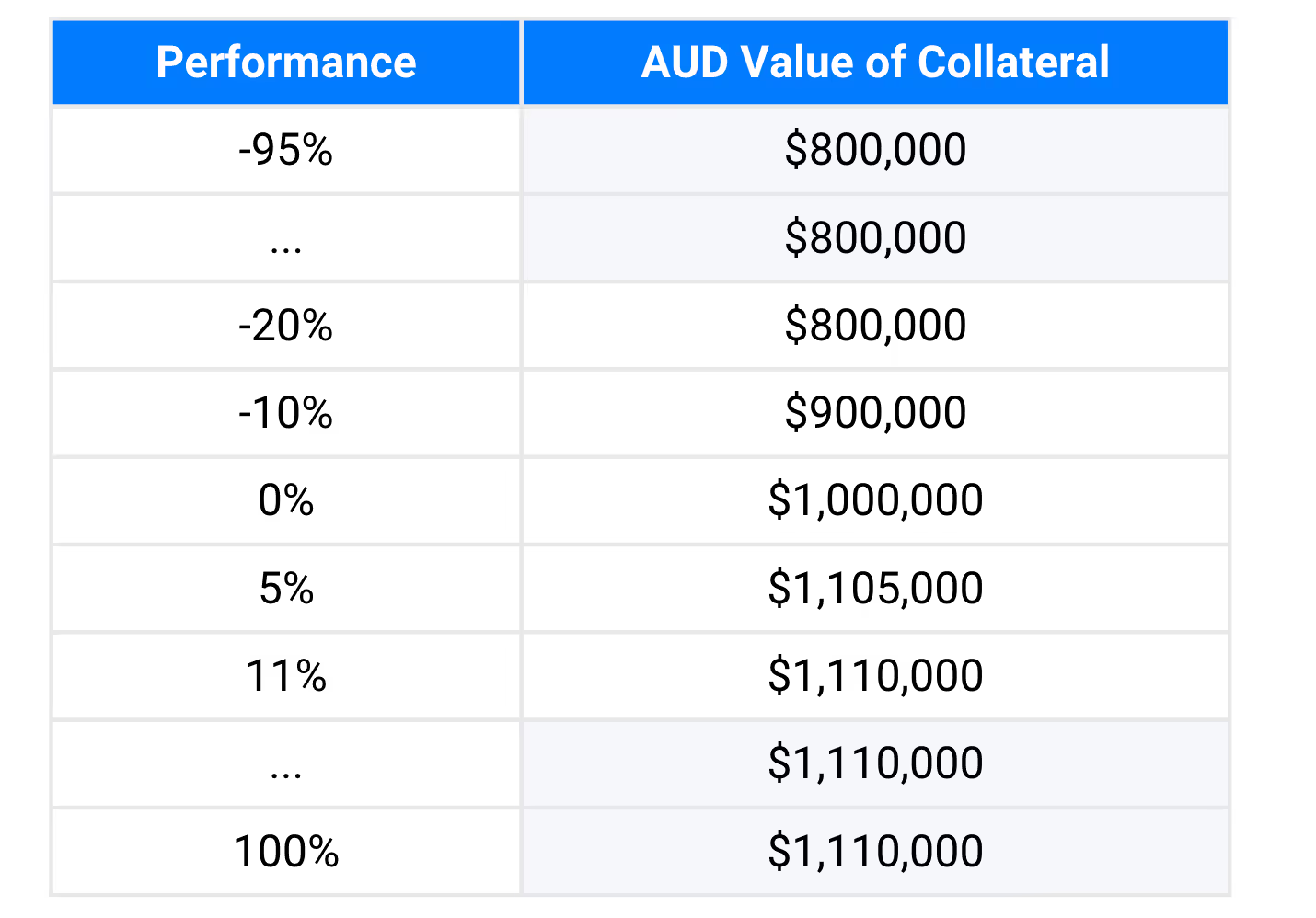

Investor have the option to liquidate shares at expiry. This amount can then be used to settle the loan obligation. Payout table illlustrated below.

1. Subject to the credit risk of the issuer.

2. Wholesale investors only. All figures are illustrative. Review the issuer’s docs and seek tax/financial advice.

3. Product terms and pricing are indicative only and subject to change.

4. Product terms and pricing are indicative only and subject to change.

.png)