.png)

After three strong years for US equities, the question for 2026 is less “will it keep rallying?” and more “what needs to go right for it to continue?”

When markets are near highs, clients don’t need more predictions. They need clear trade-offs, decision rules, and structures that help them stay invested when experts disagree.

That’s why Stropro built our Annual Institutional Outlook 2026: an evidence-first synthesis of 15+ institutional outlooks designed for private wealth advisers, designed to show where major institutions align, where they diverge, and what that implies for portfolio decisions, without relying on any single house view.

For clients: “The big debate in 2026 isn’t whether risk assets work. It is how to stay invested when experts disagree on the path.”

Adviser note: This is the public summary. Stropro advisers can request the full research-evidence pack (theme-indexed citations + tables). If you want us to map the calls to your client positioning and implementation, book a consultation with the team.

Methodology

Every outlook reflects a house view, and assumptions. To reduce single-source bias, we extracted and cross-referenced themes across 15+ institutions using hundreds of citations, grouped by theme. The goal is not to predict a single path. It is to identify where the market’s best-resourced teams agree, where they disagree, and what that implies for portfolio construction decisions.

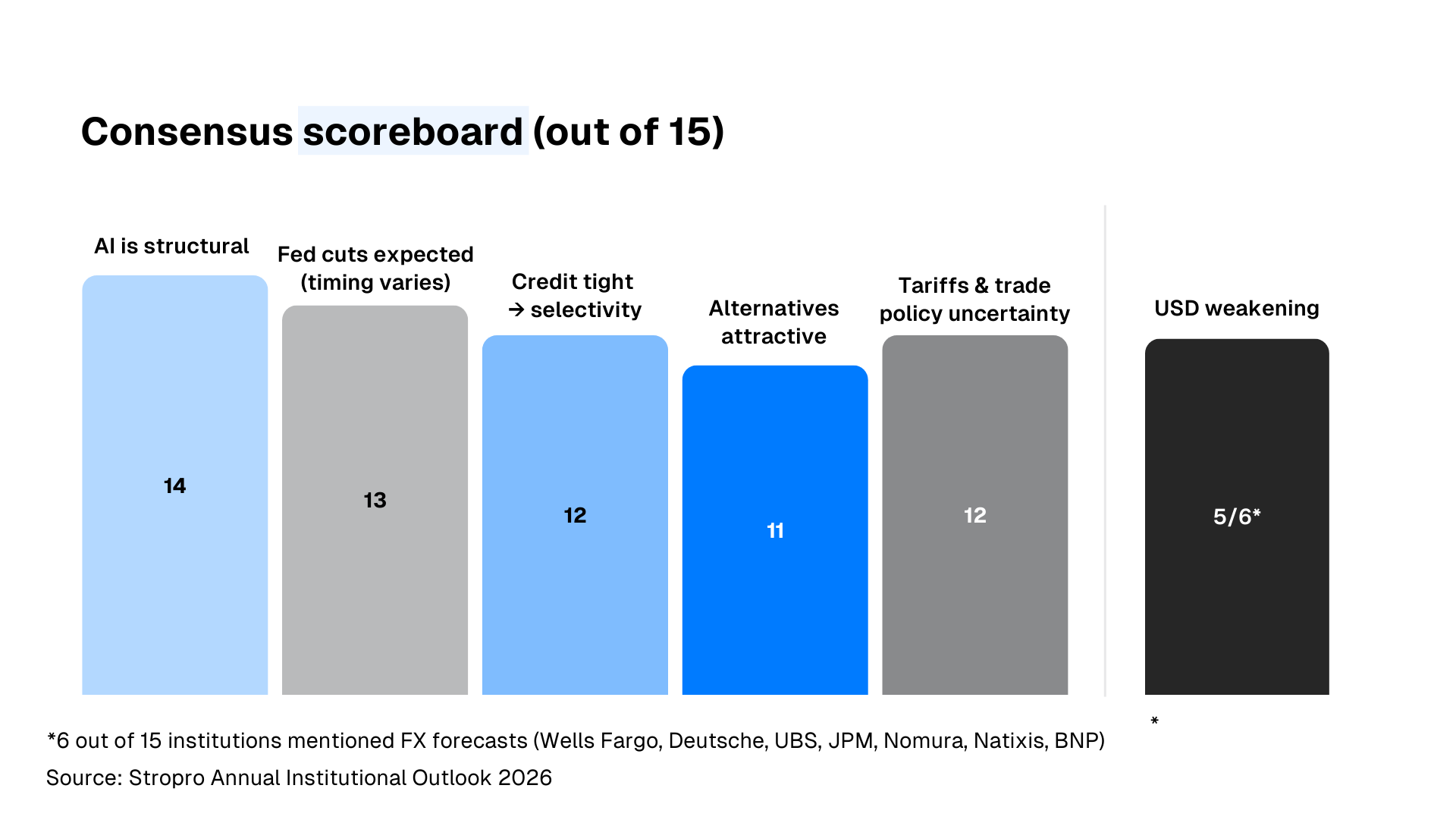

I. The Consensus Views (where houses agree)

1) The overarching theme this year: AI is structural (14/15 institutions)

AI is widely treated as a long-term investment theme, even among teams that are cautious near-term. The most repeated constraint is not chips. It is power and grid capacity. (BlackRock pp.9–11; S&P pp.4–5)

2) Fed cuts are likely (directional, not a velocity call) (13/15 institutions)

Most outlooks lean toward cuts in 2026. Timing and pace vary materially across houses.

3) Credit spreads are tight. Selectivity matters (12/15 institutions)

The repeated message is that yield is attractive, but not cheap, and dispersion is where outcomes are decided. Advisers should expect more emphasis on quality, covenant strength, manager selection, and structure.

Where relevant, it is helpful to distinguish:

- Listed credit: spreads, liquidity and mark-to-market behaviour

- Private credit: dispersion, underwriting standards, manager selection, and liquidity terms

4) Alternatives remain relevant as diversifiers (11/15 institutions)

Many outlooks still like alternatives, but the takeaway is that diversification is not automatic, especially if liquidity and drawdown behaviour are misunderstood.

5) Geopolitics: Tariffs and trade policy uncertainty dominate (12/15 institutions)

The most consistently flagged geopolitical risk is tariffs and trade-policy uncertainty, mainly because it feeds directly into inflation, margins, and cross-border capex decisions. Several houses also frame economic nationalism as a multi-year regime shift rather than a one-off shock.

- Tariff pass-through to consumers expected to continue (~70% by YE26 per Morgan Stanley IM)

- Small companies more vulnerable to tariff uncertainty (Wells Fargo)

- US Supreme Court ruling on IEEPA for tariffs could affect ~70% of tariff revenue (UBS)

- Economic nationalism described as "defining landscape shift" (JPM LTCMAs)

- The tariff environment will be moving toward 2026. Their institutional survey says 65% project increased defense spending; 77% Europe, 81% North America bullish on defense stocks (Natixis)

6) USD weakening consensus: 5 out of 6 institutions

Key mentions:

- USD viewed as overvalued and set to weaken further (JPM LTCMAs)

- USD/JPY targets imply a weaker USD versus current levels: 145 to 148-152 targets (weaker USD from current 156) (Wells Fargo, Deutsche)

- Euro expected to appreciate vs USD; yen appreciation limited despite weaker USD (Nomura)

- EM nations with tech sectors stand to benefit from lower US yields and weaker dollar (BNP Paribas)

- weakening USD makes EM more attractive (Natixis)

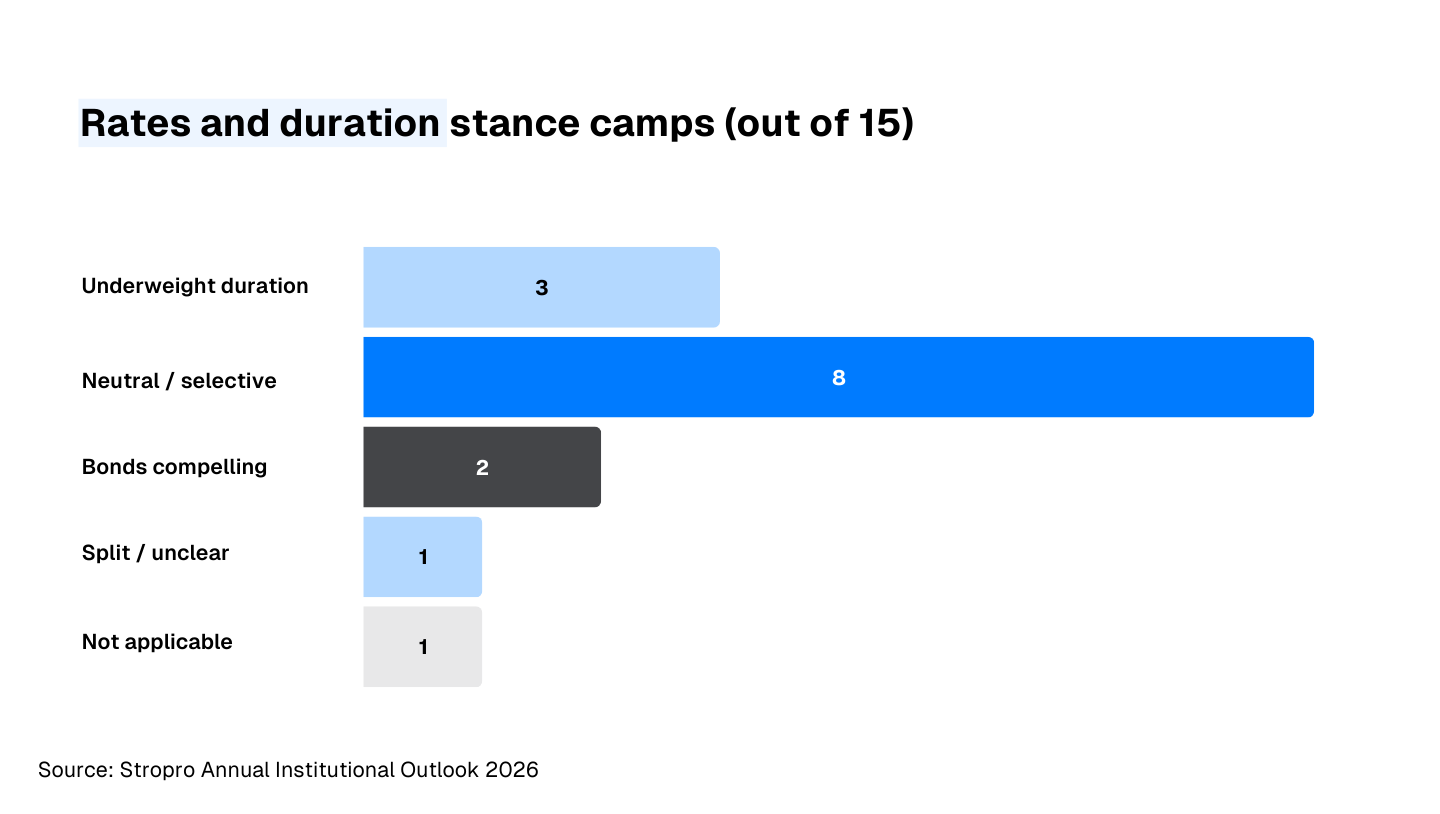

II. The Contested Views (where institutions disagree most)

1) Duration and Fed sequencing

Across institutional outlooks, rates and duration are the clearest fault line for 2026.

- Underweight duration: BlackRock; Morgan Stanley IM; Citi

- Neutral / selective: Barclays; Macquarie; GSAM; UBS; Deutsche; BNP Paribas; Nomura; Wells Fargo

- Bonds compelling: Vanguard; J.P. Morgan AM (LTCMAs)

- Split / unclear: Natixis (survey-based split)

- Not applicable: S&P (theme-specific energy trends)

Some houses argue investors should remain underweight duration, citing fiscal risk, term-premium uncertainty and sticky inflation. Others argue “bonds are back”, pointing to real yields and diversification benefits. A large group sits in between, advocating selective or staged exposure.

This dispersion matters because it signals that the range of reasonable outcomes is wide.

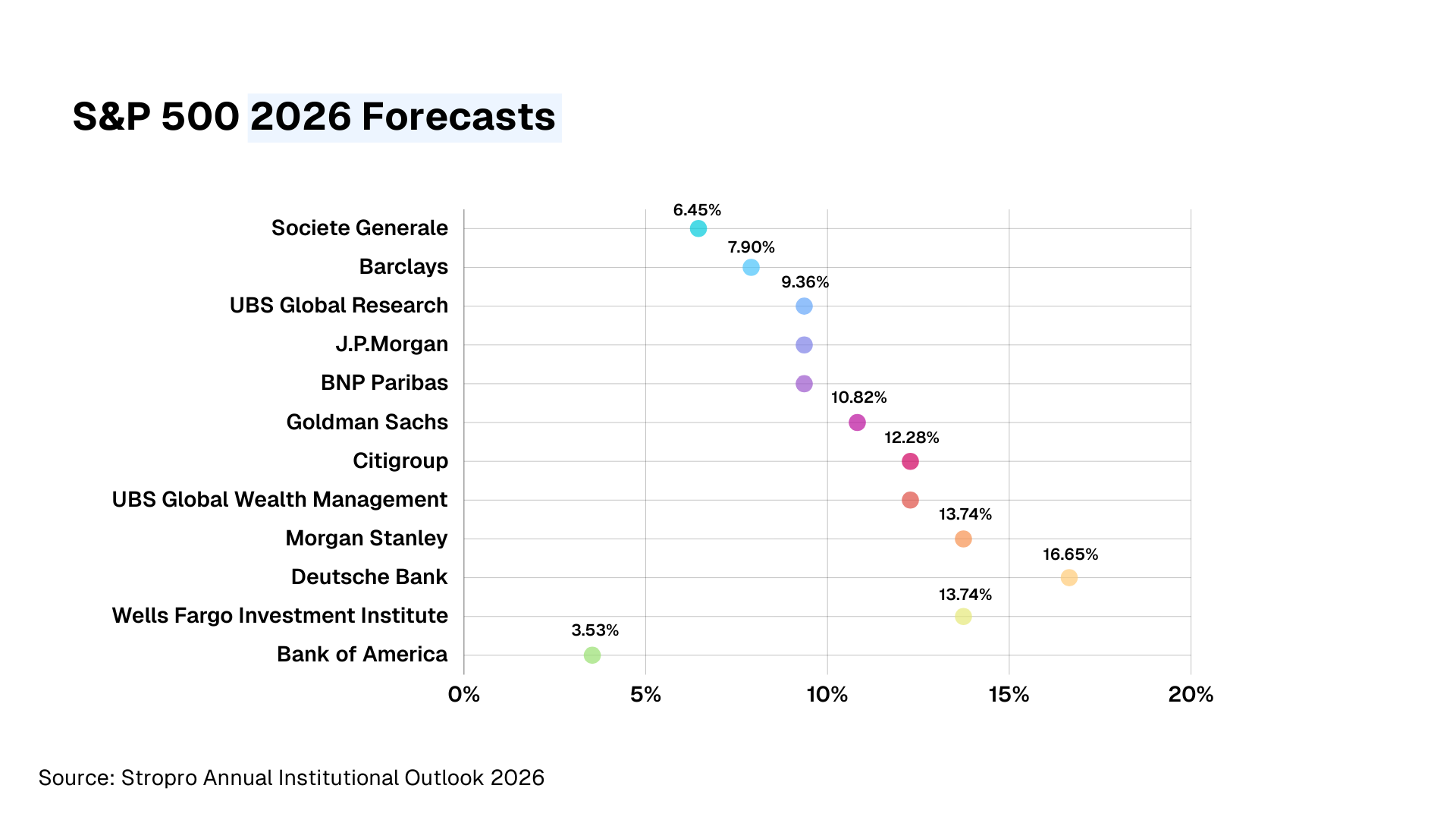

2) S&P 500 year-end targets

Predictions for year-end 2026 range from:

- Most Conservative: Bank of America at 7,100 (3.53% gain)

- Most Optimistic: Deutsche Bank at 8,000 (16.65% gain)

- Median Forecast: 7,700 (10.09% gain)

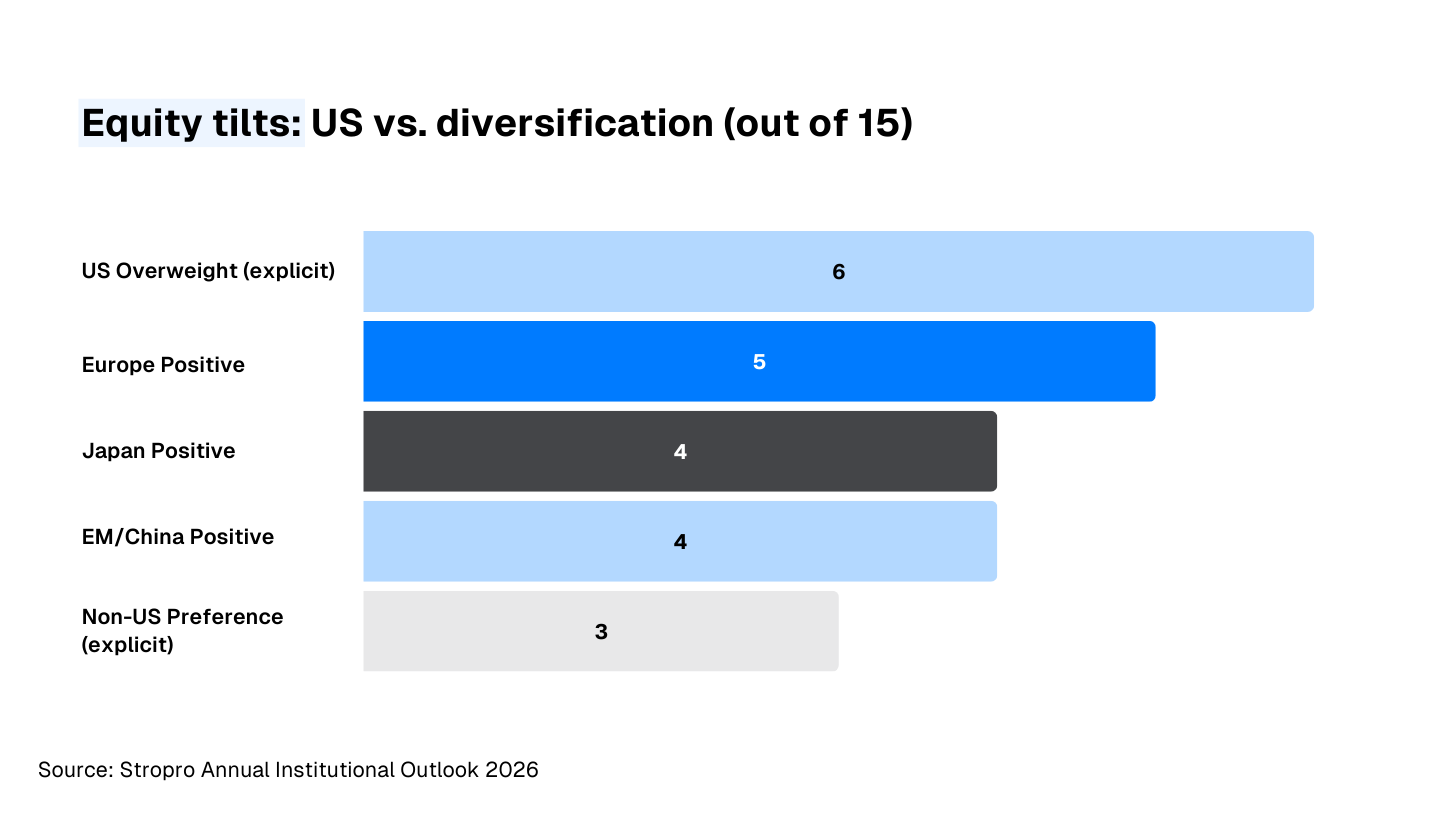

3) Equity regional tilts: US core, diversification louder

Most outlooks keep the US as a core equity allocation, but a meaningful subset emphasises diversification (valuations and concentration) and or tilts to Europe, Japan, and parts of EM on relative value.

“The debate isn’t whether the US stops being important. It is whether one market needs to do all the work in 2026.”

Common rationale:

- US: earnings quality and AI leadership

- Non US: valuation support, policy tailwinds, or currency effects

- Balanced: keep core US exposure but add selective international allocations

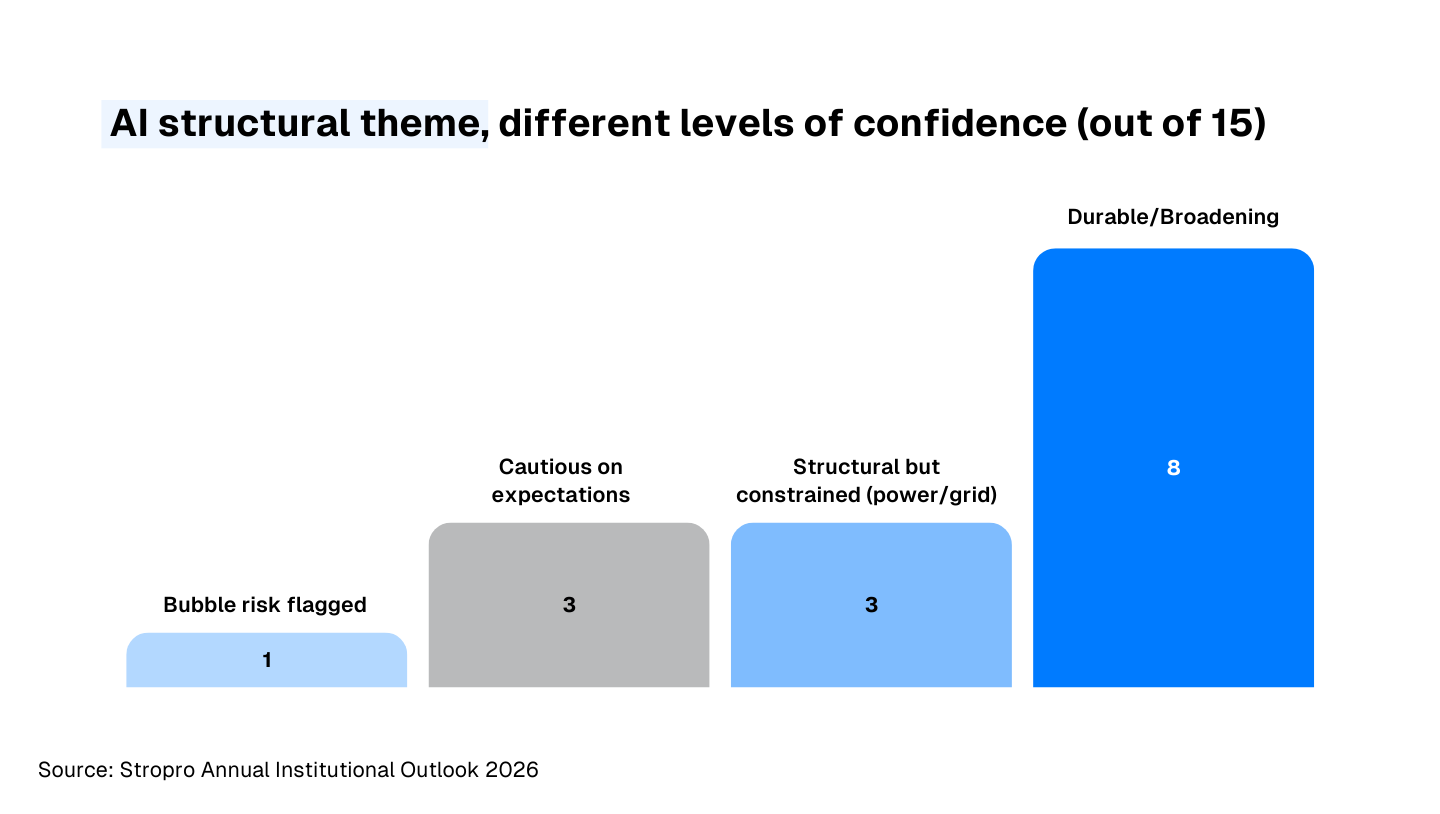

4) AI, different levels of confidence.

AI is close to a universal macro and equity driver in the outlook set. Divergence appears in sustainability and the near-term path:

- Constraints: power and grid, regulation, physical buildout

- Valuations: crowded leadership, high expectations

- Timing gap: capex now vs revenues later

Portfolio framing, Instead of “Do we own AI?”, many outlooks implicitly separate AI beneficiaries:

- Beneficiaries (platforms, software, semis)

- Enablers (power, grid, data centres, select industrials)

- Adopters (sectors where productivity shows up in margins)

That framing helps investors avoid binary thinking and reduces the “Mag 7 or nothing” trap.

III. Stropro Investment Desk: Portfolio Implications (how advisers translate disagreement into rules)

1) Duration: the issue is path risk, not just direction

When a call is genuinely contested, the risk is not being wrong on rates. The risk is building portfolios that only work if one path occurs. Rather than choosing a camp, advisers can design exposure that behaves sensibly across outcomes.

If rates stay higher: Avoid excessive long-duration risk. Prioritise carry, income, and shorter tenors.

If rates fall meaningfully: Retain some duration participation to capture diversification and capital upside.

The common thread is not prediction. It is portfolio resilience.

When duration is contested:

- Avoid single-bet positioning

- Layer exposure over time

- Align investment tenors with client horizons

- Use defined payoffs so downside behaviour is known in advance

This is why advisers increasingly favour rule-based, defined-outcome approaches when macro conviction is split.

2) Equities: concentration and breadth matter more than “US vs not-US”

Portfolio reviews become less about “US vs not-US” and more about concentration risk, breadth of earnings, and valuation discipline.

Implementation can shift toward defined entry levels, pre-agreed downside rules, and broader underlying selection (indices, ETFs, sectors) so clients do not feel they must pick a single winner.

3) Credit and alternatives: diversification is not automatic

Across outlooks, the repeating credit message is consistent:

- Spreads are tight. Quality and structure matter.

- Private credit dispersion is rising. Manager selection and underwriting matter.

- Investors want yield, but not “mystery risk”.

Many outlooks still like alternatives for diversification, but the message is that alternatives do not automatically protect you. The real questions are:

- What happens in a drawdown?

- How liquid is it?

- How transparent is pricing?

- What is the cashflow profile?

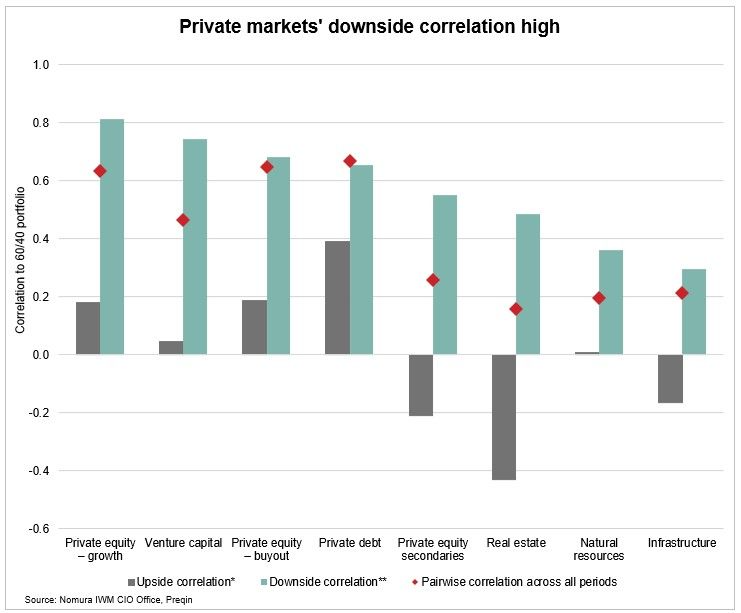

In our Adviser Trends Sep Q3 2025, we highlighted that many alternative allocations have shown higher correlation to equities than expected, and that correlations tend to increase during downturns (see chart below).

Many advisers are also using structured investments as a complementary tool. While these strategies can still be correlated to equity markets, their transparent payoff profiles, explicit downside-protection settings, and shorter tenors (typically 6–24 months) can make them a more reliable portfolio implementation tool when conviction is split.

When experts disagree, you don’t need a prediction. You need rules.

When outlooks conflict, clients lose confidence. They hesitate at highs and panic in drawdowns. Advisers are partnering with Stropro to replace forecast talk with portfolio rules.

That’s exactly why defined-outcome structured investment solutions have been used more in practice:

- “Get paid while we wait” smart-entry income note style structures

- income with explicit buffers

- growth exposure with protection settings and guardrails

- shorter horizons and frequent resets when markets change

Enjoyed these insights?

If this summary was useful, you’ll probably like our ongoing research and adviser trends cadence. Book a consultation with the Stropro Investment team or subscribe below to get our latest institutional outlook summaries, market themes, and adviser implementation insights as they evolve through 2026.

How Stropro supports advisers

Unlock the access, support, and technology required to manage modern portfolios with confidence.

Our process:

- Discovery and Ideation

- Optimisation and Price Tendering

- Execution and Compliance

- Enhanced Lifecycle Management on our Adviser Hub

- Integration with your existing tech stack

Appendix: Source library (15 documents)

Barclays Private Bank Outlook 2026: The Interpretation Game

BlackRock Investment Institute 2026 Global Outlook

Macquarie 2026 Investment and Economic Outlook

Morgan Stanley IM The BEAT Q1 2026

Goldman Sachs AM Investment Outlook 2026

Citi Wealth 2026 Q1 Macro Investment View

UBS CIO GWM Year Ahead 2026: Escape Velocity?

Deutsche Bank WM Perspectives 2026 Annual Outlook

BNP Paribas AM Investment Outlook for 2026

Vanguard Economic and Market Outlook for 2026

J.P. Morgan AM 2026 Long-Term Capital Market Assumptions

Nomura AM Investment Outlook Winter 2026

Natixis IM 2026 Institutional Outlook Survey

Wells Fargo Investment Institute 2026 Outlook: Trendlines over Headlines

S&P Global Energy Horizons Top Trends 2026

Important Information:

1. Wholesale Investors only.

2. Subject to credit risk of the issuer.

3. Tax outcomes depend on individual circumstances and applicable tax law, and may be subject to change. Investors should seek independent tax advice regarding CGT deferral and interest deductibility.

Investments made available on the Stropro platform are only available to wholesale, sophisticated or professional investors and their financial advisers. Information is general in nature. Please consider whether the information and investments are suitable for you and your personal circumstances. Stropro Operations Pty Ltd (ABN 28 633 603 399) (Stropro) is a Corporate Authorised Representative (CAR No. 1293257) of Stropro Compliance Pty Ltd (ABN 74 640 214 740, AFSL No. 533443). Stropro Operations Pty Ltd and Stropro Compliance Pty Ltd are subsidiaries of Stropro Technologies Pty Ltd (ABN 80 619 399 932). © 2025.